Understanding Managerial Accounting (Controlling (CO)) in SAP FICO

In our previous article, we explored Financial Accounting (FI), which focuses on external reporting. In this article, we’ll consider the “CO” in FICO: Managerial Accounting, also known as Controlling.

Thank you for reading this post, don't forget to subscribe!What is Managerial Accounting (Controlling)?

Managerial accounting is designed to collect data for the preparation and analysis of reports for use by internal users within an organization. Unlike financial accounting, which provides data for year-end reports (balance sheets, income statements, general ledger accounts) for external users, in controlling, reports are prepared based on the collection of data for internal users.

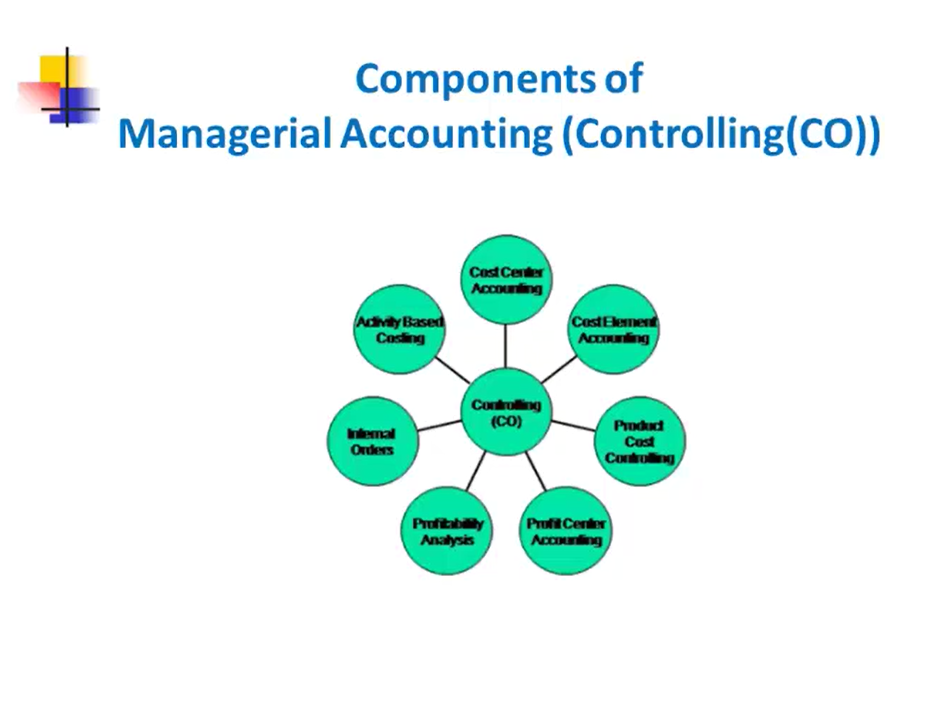

The components of Controlling (CO) include cost center accounting, cost element accounting, product cost controlling, profit center accounting, profitability analysis, internal orders, and activity-based costing.

Controlling Reporting

Controlling reporting involves providing internal management with detailed reports by cost center or other cost objects, as well as cost elements. The key aspect includes:

- Cost Centers

- Orders and Projects

- Budget/ Plan

- Actual vs. Plan

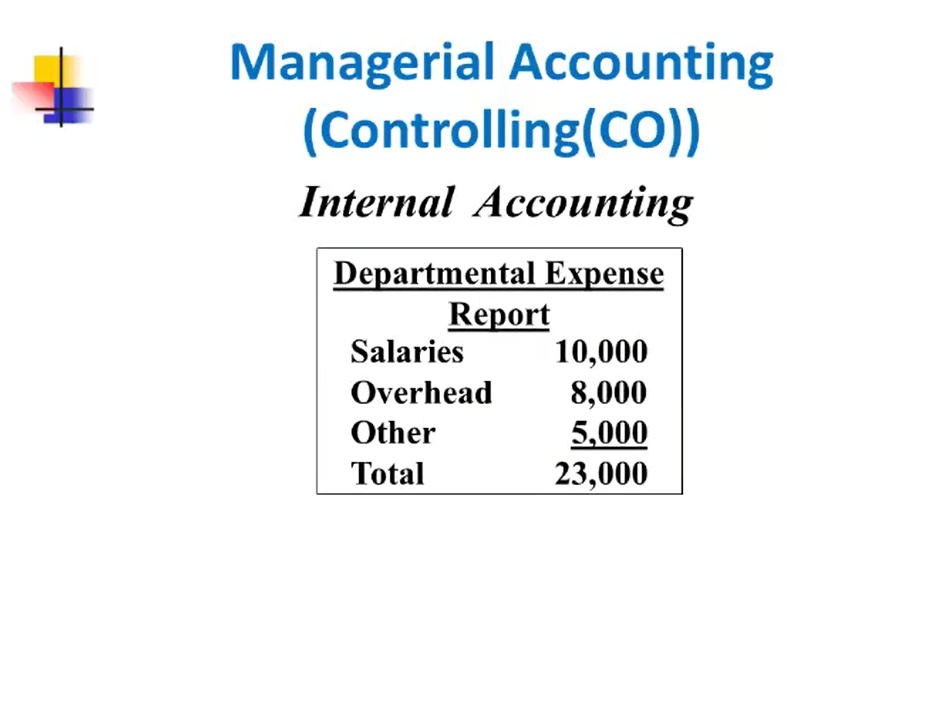

For example, consider a departmental store’s internal accounting in the image below:

It contains the expense report based on salaries, overhead, and other expenses, with a total outcome of 23,000 for that particular departmental store. Here, we have internal users such as controllers, senior management teams, departmental managers, and executives, who manage and utilize the expense report for the departmental store.

Financial Accounting vs. Managerial Accounting (Controlling)

Below is a comparison between Financial Accounting (FI) and Controlling (CO):

| Financial Accounting (FI) | Controlling (CO) |

| Legal or external reporting | Internal management reporting |

| Reports based on accounts, balance sheet, and income statement | Reports based on cost centers, cost elements, and cost center reports |

| External users (investors, regulators, etc.) | Internal users (management, department heads) |

This comparison highlights the differences between Financial Accounting and Controlling.

Organizational Structure in SAP

Organizational Data:

- A hierarchy in which the organizational units in an enterprise are arranged according to tasks and functions.

- Static data and is rarely changed.

- The definition of organizational units is a fundamental step; it is a critical factor in how the company will be structured.

Elements of Organizational Structure

The organizational structure in SAP FICO CO comprises several elements:

- Client

- Company

- Chart of Accounts

- Company Code

- Fiscal Year Variant

- Business Area

- Credit Control Area

- Controlling Area

- Integration with other modules

Client

The client is the most important and highest hierarchical level in an SAP system. It is a complete database containing all the tables necessary for creating a fully integrated system. Master records are created at the client level, meaning they are accessible across all company codes and other organizational units within that client.

Company

A company in SAP represents a legal entity for which consolidated financial statements are created. It has company codes that define the financial statements of the company. A single company can include one or more company codes, but all company codes belonging to the same company must use the same chart of accounts and fiscal year variant.

Chart of Accounts

The Chart of Accounts is a list of all the accounts used by a business. There are five types of accounts contained in a chart of accounts:

- Assets

- Liabilities

- Equity

- Revenues

- Expenses

These accounts were covered in our previous article on financial accounting. There are two primary accounting reports prepared from the general ledger:

- Balance Sheet – comprises assets, liabilities, and equities

- Income Statement – comprises revenues and expenses, i.e., profit and loss statements