Asset Accounting 4

So we need to assign the GL accounts. For the GL account that whatever you have created in yesterday’s class, all those things we are going to integrate with asset accounting. The path is going to be financial accounting (new), asset accounting, integration with general ledger accounting, assign GL accounts. AO90 is the T code for this. So choose a chart of depreciation. We have already created the chart of depreciation that is DRCD. .

Thank you for reading this post, don't forget to subscribe!

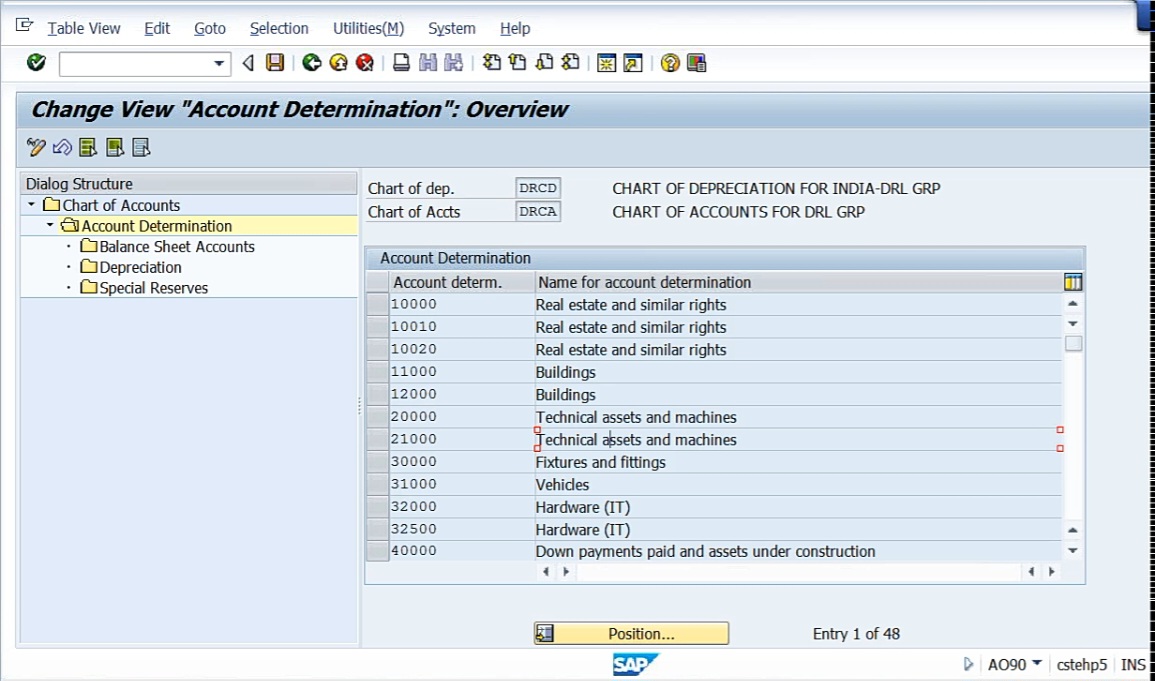

So this is the chart of accounts for DRL group, and DRCD is the chart of depreciation. So both of these integrated with each other. Now what we do, whatever the GL account that we have created, those GL accounts, few are balance sheet accounts, few are depreciation accounts. Let us select DRCA, double click on account determination, it will show you the account determination.

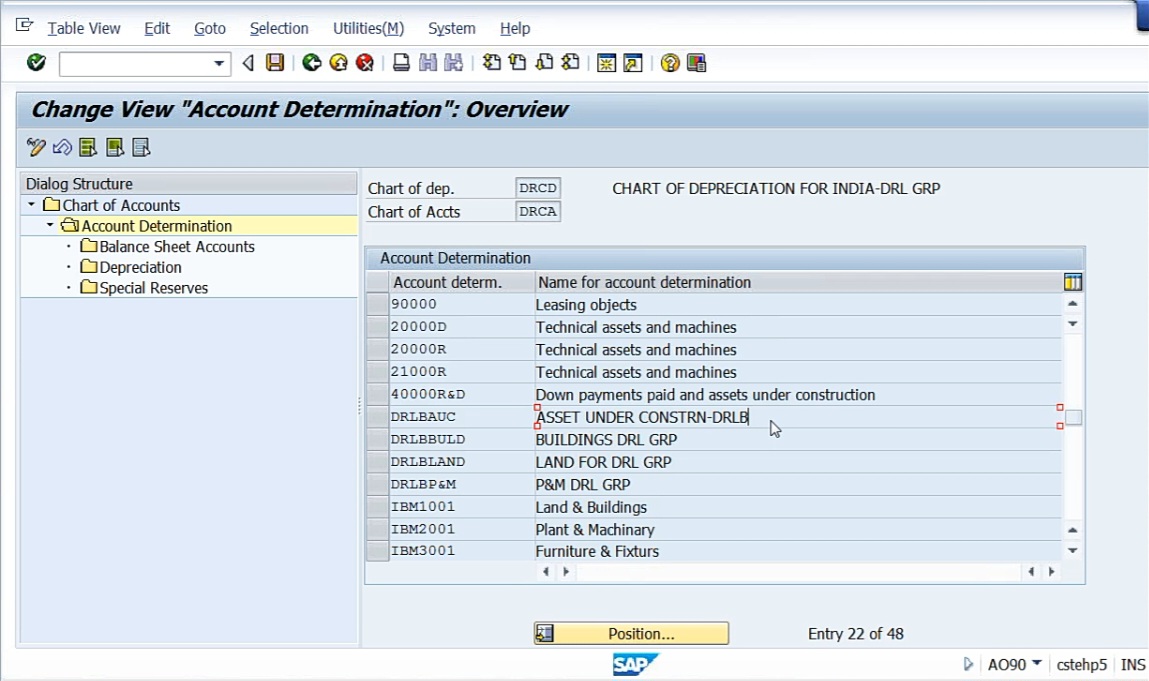

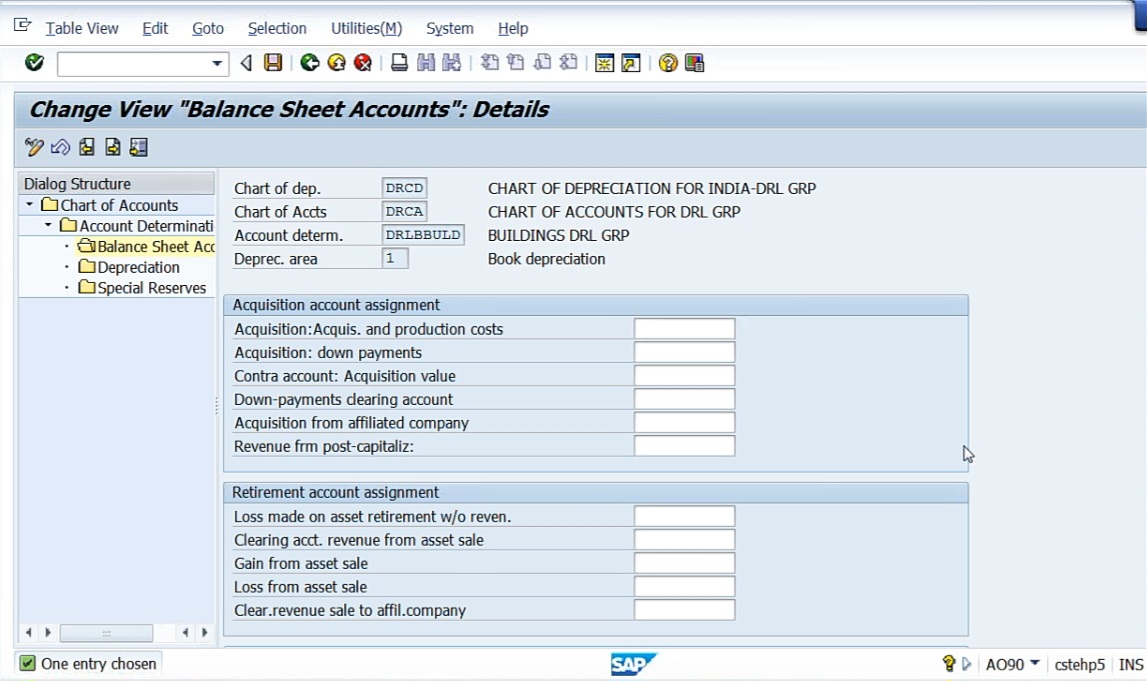

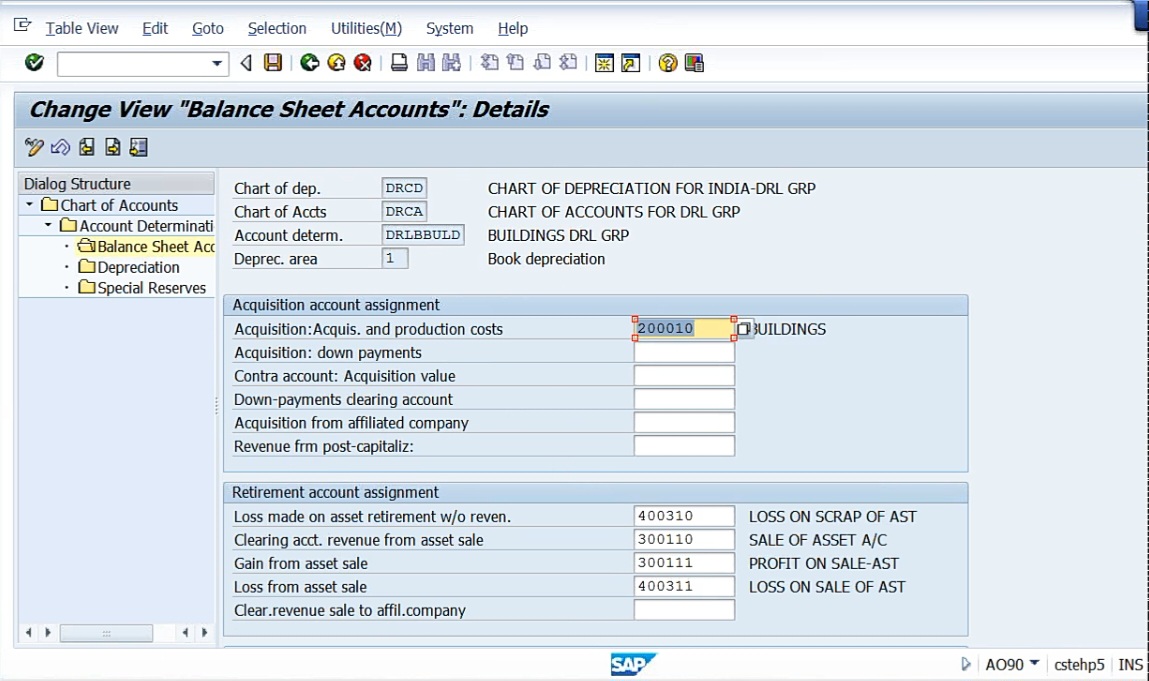

So these are the account determination we have already created. There is DRLBAUC, that is asset under construction. There’ll be building, land, plant and machinery. So all these things we have already created. Now what we need to do, we need to assign the GL accounts for each and everything. Say for example, you take buildings. Select DRL Buildings, double click on balance sheet account.

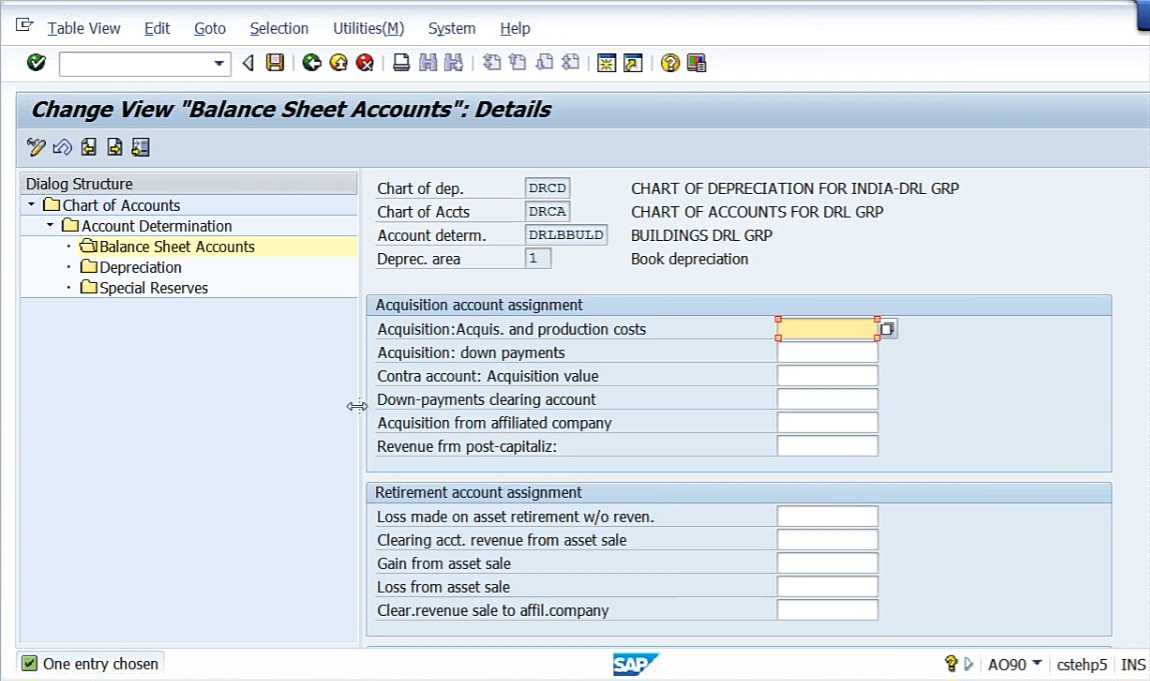

So here we need to assign in case if you are going to procure an asset to which account it has to be posted. So in case of asset accounting, whenever you are going to procure an asset, whenever you want to sell an asset, whenever you want to provide depreciation, everything is automatic. Here, we are not going to post any entry manually. So everything will be triggered automatic line items. Let us see how we are going to do it. Now let us integrate the first. Here, what we are telling to the system in case see acquisition, acquisition and production costs means for buildings, DRL buildings, if I’m going to acquire or produce, these things should be debited to which account?

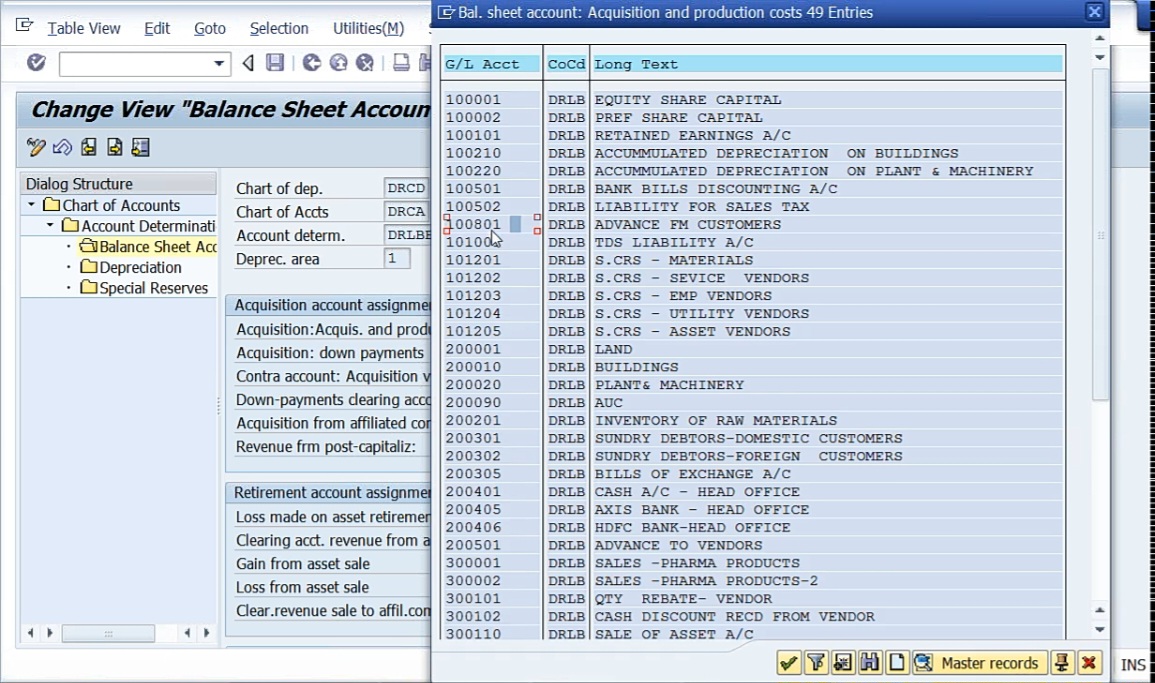

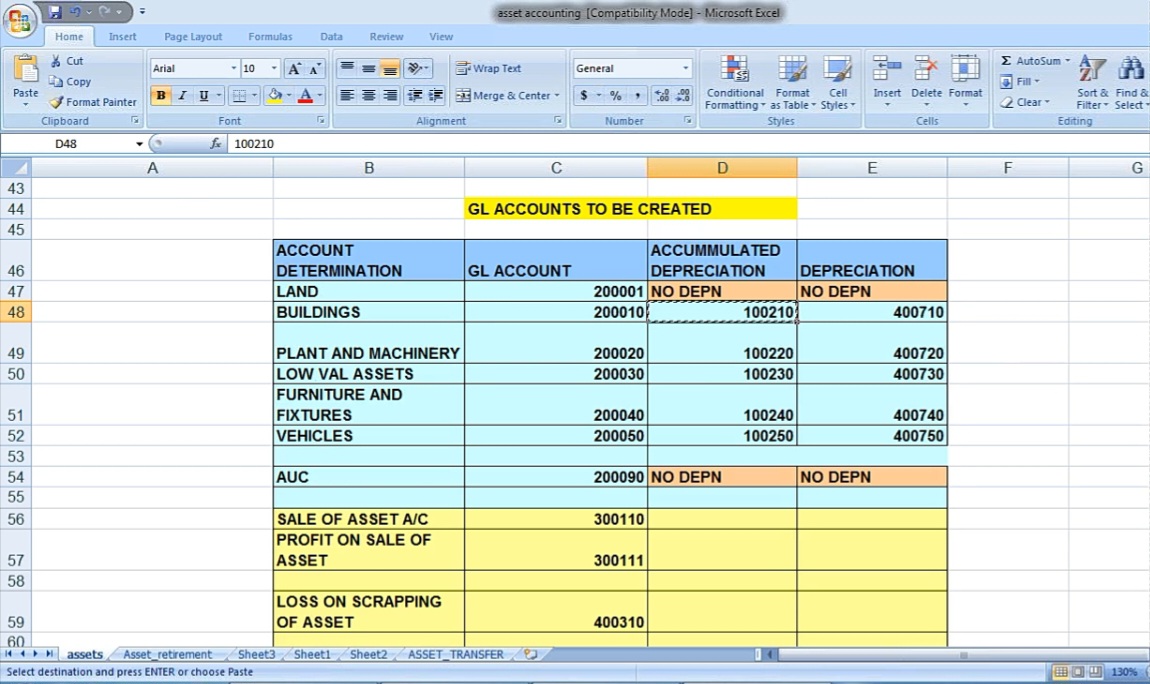

See buildings GL account 2 lakh 10. So acquisition.

So we are telling the system, in case I’m going to procure an asset, post to this account and all these things you can drill down and you can see here.

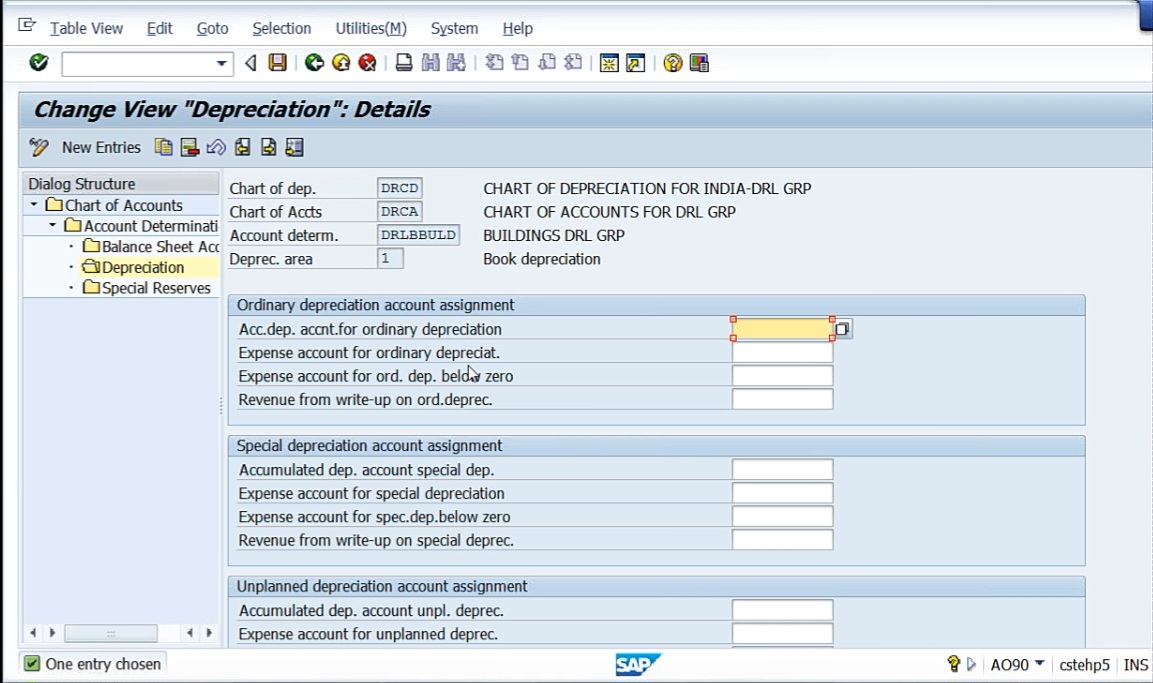

Land, building, plant and machinery, AUC. So in case if you are going to acquire a building, it should be posted here. Now retirement account assignment, these are the things which are not required as of now. Retirement account assignment means in case if I’m going to return my asset. Retirement means you sell away, or scrap it anyway. Now loss made on asset retirement without revenue. So without revenue means, see when you are going to get the loss on asset retirement without revenue, that is nothing but when you scrap one particular asset. In case if you are going to scrap it, to which account it should be posted. Similarly, clearing account, revenue from asset sale, gain from asset sale, loss from asset sale. Now loss made on asset retirement without revenue means without revenue when you are going to get the loss that is when you scrap the account. So loss on sale of asset, loss on scrapping of the asset. When you scrap an asset, 400310. Put the GL account here. Cleaning account revenue from sale of asset, this is nothing but sale of asset account. And gain from asset sale, if you get any profit on asset sale. Profit on sale of asset, let us post here, 300111. Loss from asset sale, in case if you are going to get any loss on sale of asset, 40311. So I want the GL account to be triggered when I post these transactions I have given here. So automatically the system picks up this GL account, we need not even select GL accounts at the time of posting. So, see, it is a building, it’s a depreciable asset, we have depreciation on building. So that’s why here, in case if we are going to get any depreciation, what are the GL account that we have to use? Double click on depreciation.

This is accumulated depreciation, expense account depreciation. So I told you whenever depreciation is posted, the accounting entry is going to be depreciation account return to accumulated depreciation account. So because so many people, what they do is, depreciation account return to asset they use. It is not the asset. Here, because we have to maintain the historical value of the asset, that’s why what we need to do is, depreciation is an expenditure and accumulated depreciation is a liability, so depreciation account return to accumulated depreciation. So what is the accumulated depreciation account for building? Here we have created.

Building accumulated depreciation. 10210. Then expense account for ordinary depreciation. 400710 is expense account depreciation. So whenever we are going to post any depreciation on building, I’m telling the system to post to this account. 100210 is liability. 400710 is expenditure. So with reference to buildings, I have assigned the GL accounts.

This is balance sheet GL account. This is nothing but the retirement account assignment and these below are the depreciations.

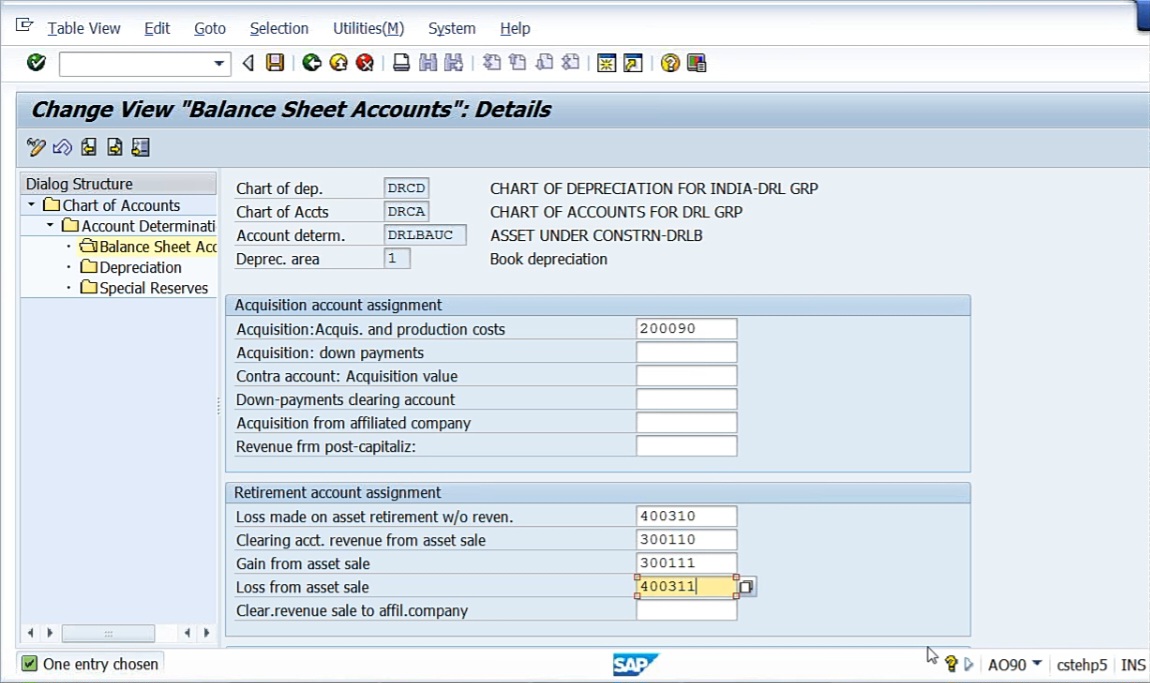

Come back to Account determination overview. So for buildings I have completed. Similarly for AUC also we can complete it. Go to Balance sheet account. AUC GL account 2 lakh 90. Other GL accounts are the same because all these are all retirement accounts.

When even AUC is retired, we have to post to the same. But in case of AUC, we’ll not have depreciation. So that’s why depreciating GL account we need not assign. Why? Because AUC’s name itself indicates that asset which is under construction. If an asset is under construction, we cannot provide depreciation unless it is complete.

Then coming to land, in case if I am going to procure land, what are the GL accounts? So land GL account is 2 lakhs 1. Same loss account and other accounts. Even here we don’t have depreciation, there’s no depreciation on land.

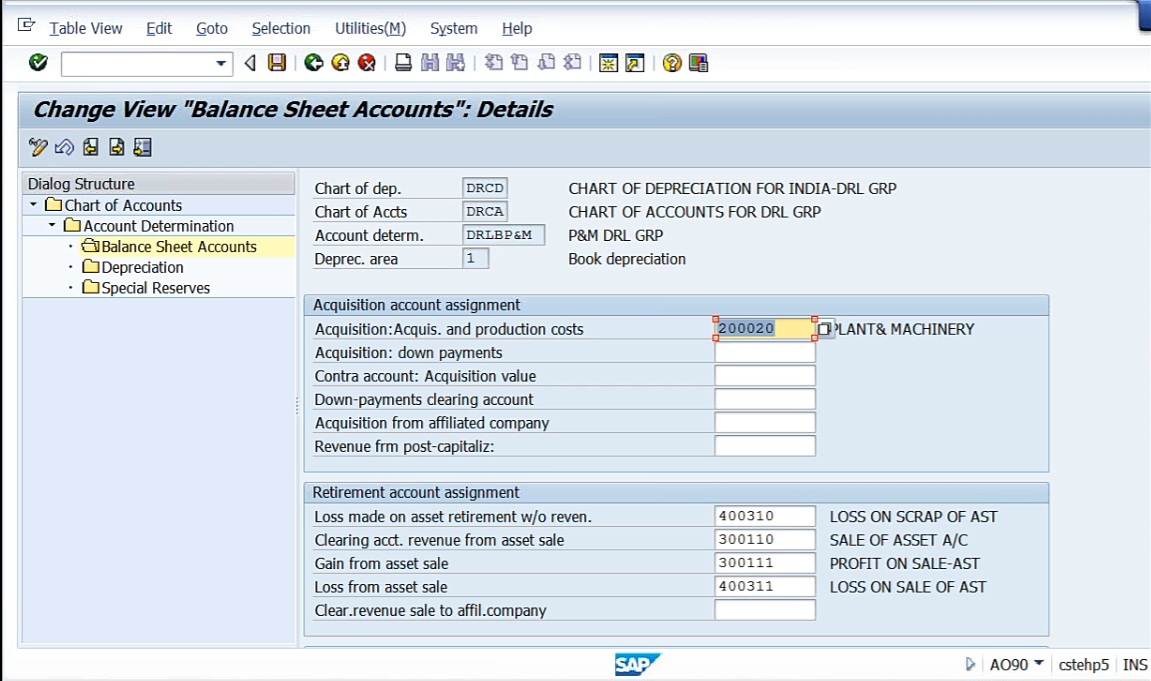

Then plant and machinery. Select it, double click on balance sheet accounts. Plant and machinery and acquisition and production costs. Plant and machinery 2 lakh 20, and retirement GL accounts are same again. Then coming to depreciation, because we have depreciation on plant and machinery. So GL account to be posted accumulated depreciation. So for plant and machinery accumulated depreciation 100220. Then the expense account depreciation 400720. So, loss on scrap of asset, sale of asset, profit on sale of asset, loss on sale of asset.

So for four (4) account determination, we have assigned GL accounts. So what are the GL account that we have assigned to, so DRLB asset accounting. So like this we have to assign the GL accounts. But this has to be done very carefully. You have to keep your body and mind together, then you have to do it. Because even if you make any smallest error here and if you post accounting entries, you cannot rectify it. So that’s why you have to be very careful while assigning the GL accounts.

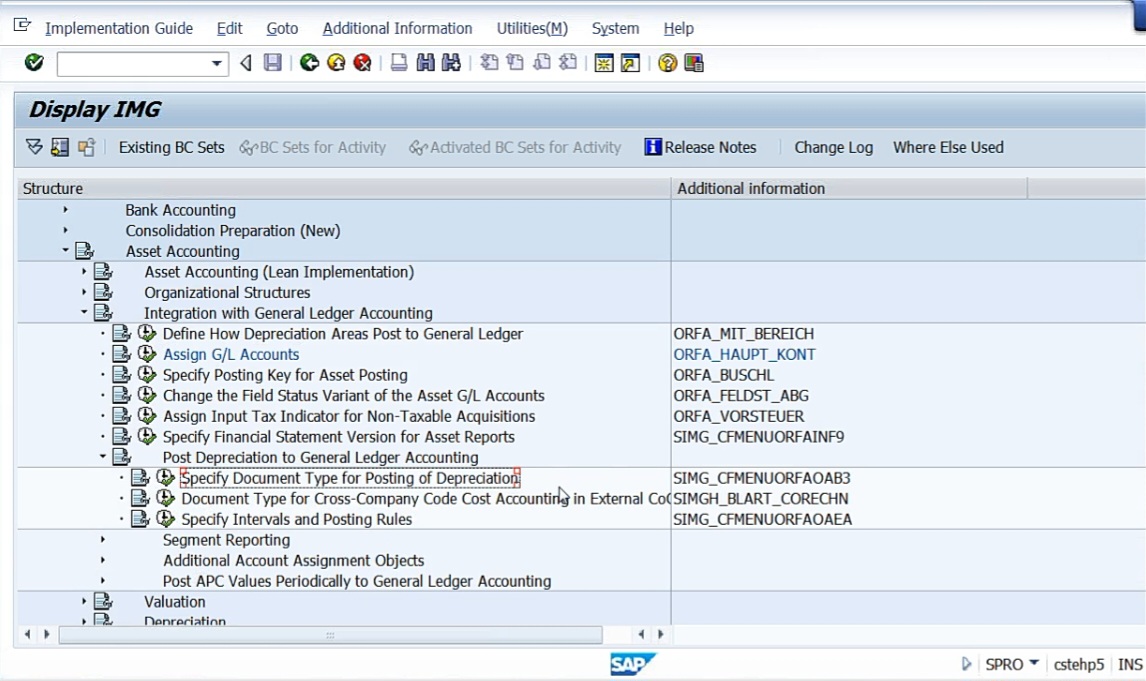

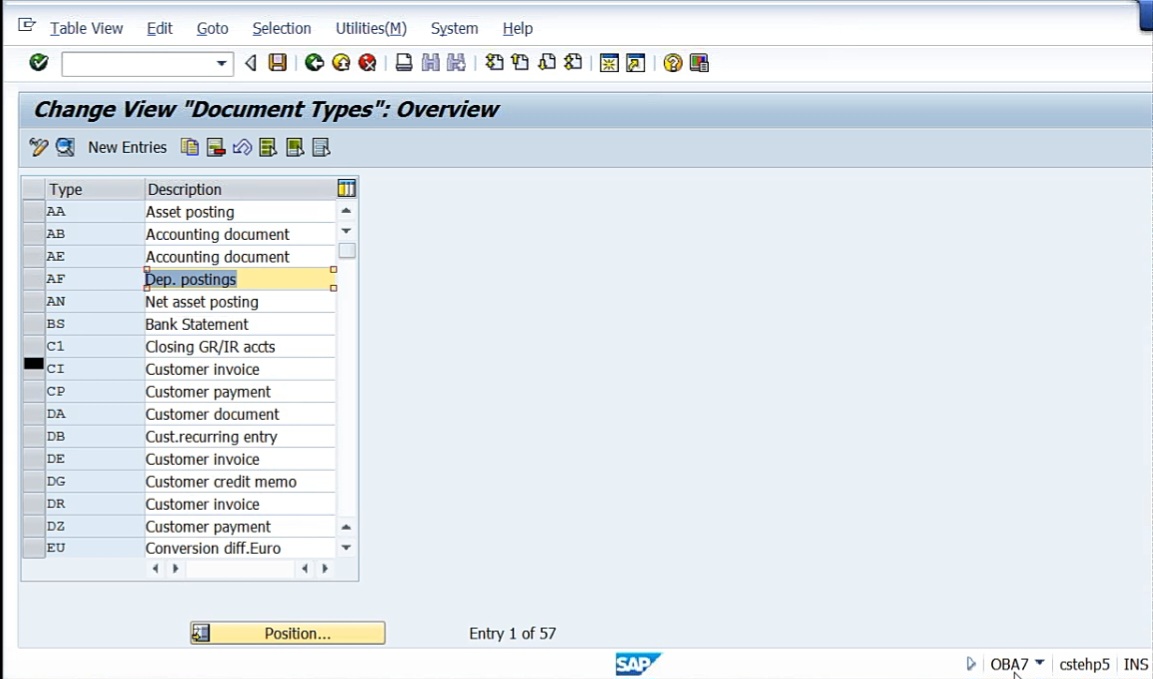

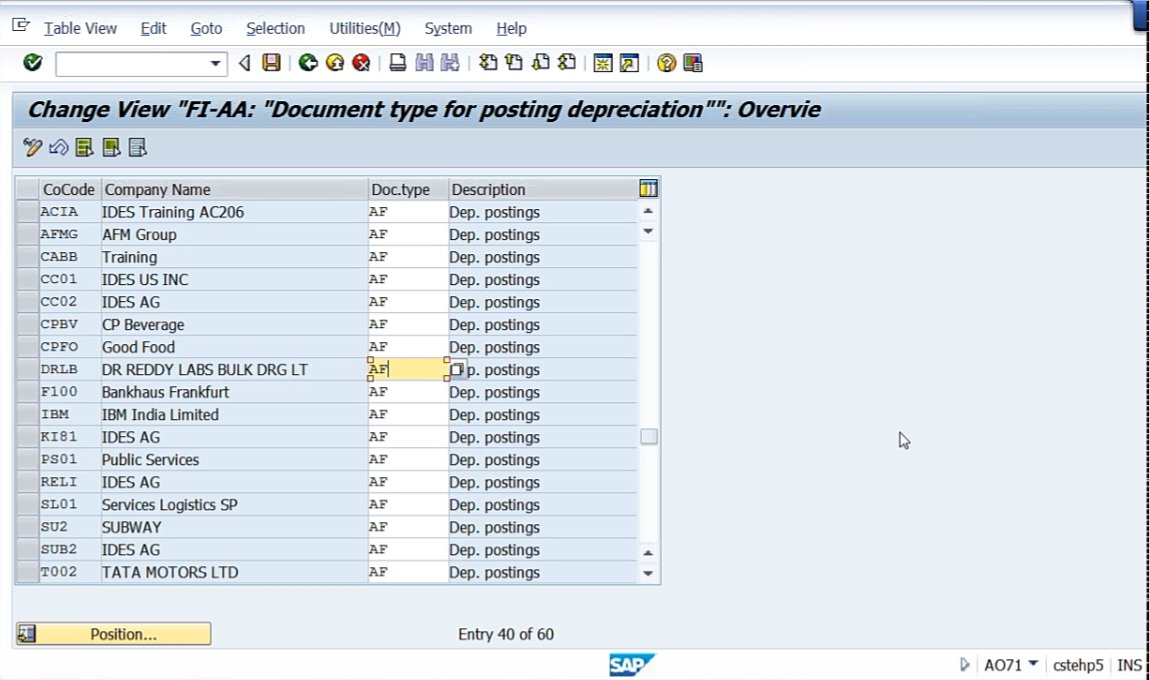

So once the integration is over, go to Specify Document Type For Posting Depreciation.

Document type, generally, AF is the document type which we use. Click Specify document type for posting depreciation. Define document type, we need not define specified document type for posting depreciation. But here, we have to assign the number ranges for depreciation posting, even depreciation, automatically system will take. That is we have to run it. So you have to run the depreciation run, then system will on each and every asset, system will post it. Select Define document types.

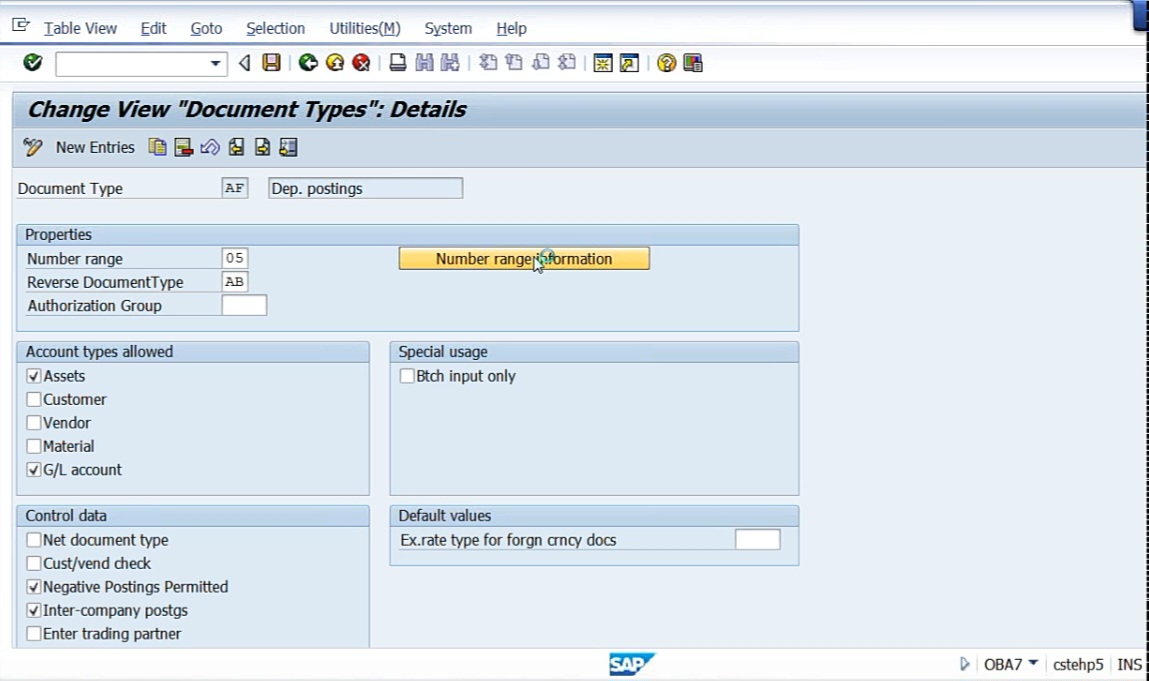

Here, AF is the document type, Depreciation postings. It will take us to again OBA7 document type. Double click on AF.

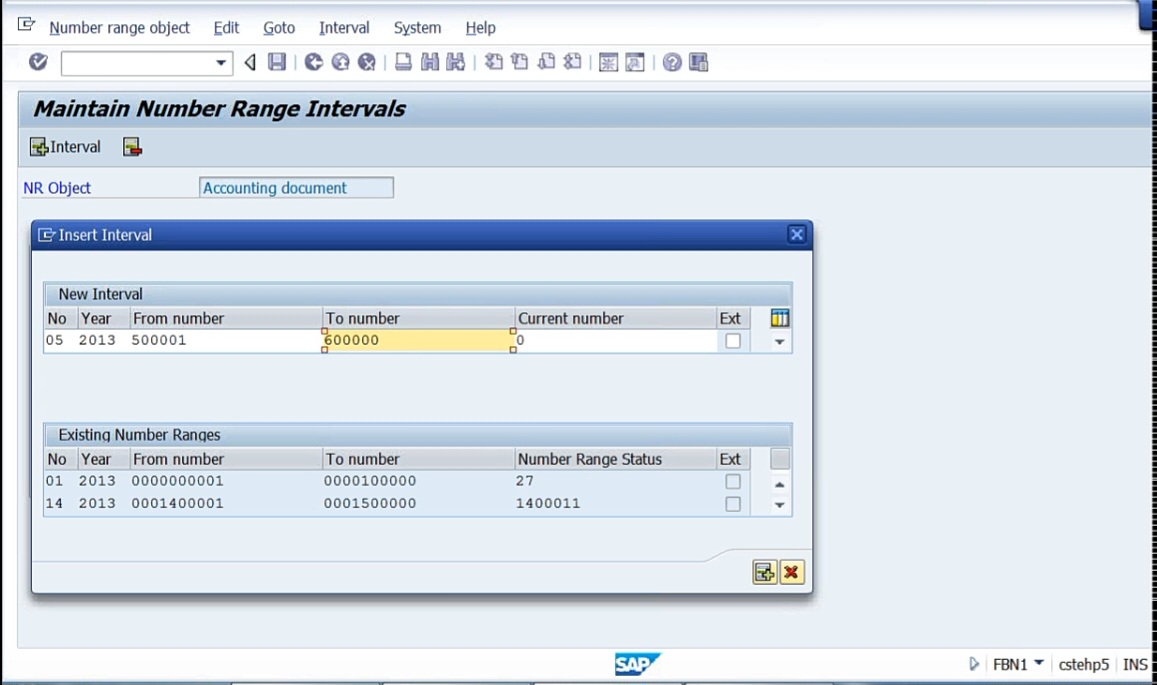

5 is the number range registered by system. Now create number range. This is for DRLB.

Click on interval, number 05, year 2013, from number 5 lakhs 1 to 6 lakhs.

Save it. So next, specify document type for posting depreciation. So we need not specify this. Automatically by default, it has been linked to the company code. You can see this.

So our company code is Doctor Reddy Labs, DRLB. See here we need not do anything. And here, we need not do anything of course, Specify Intervals And Posting Rules, not required. So that is what integration we have done it. Then coming to screen layout under master data.

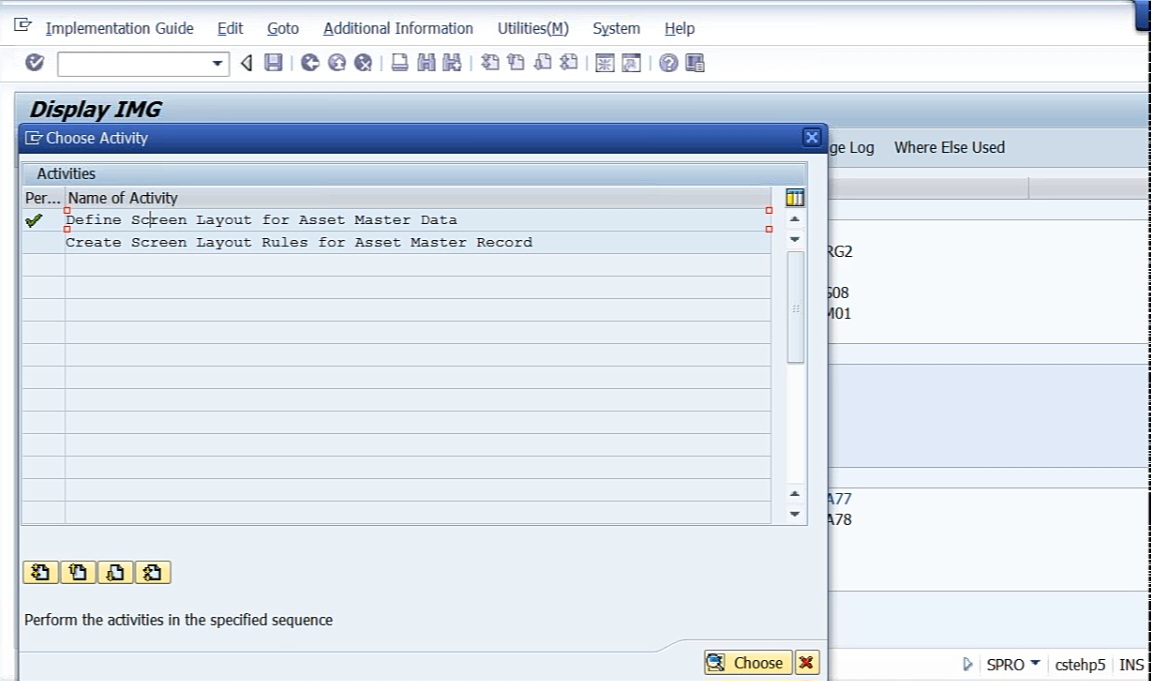

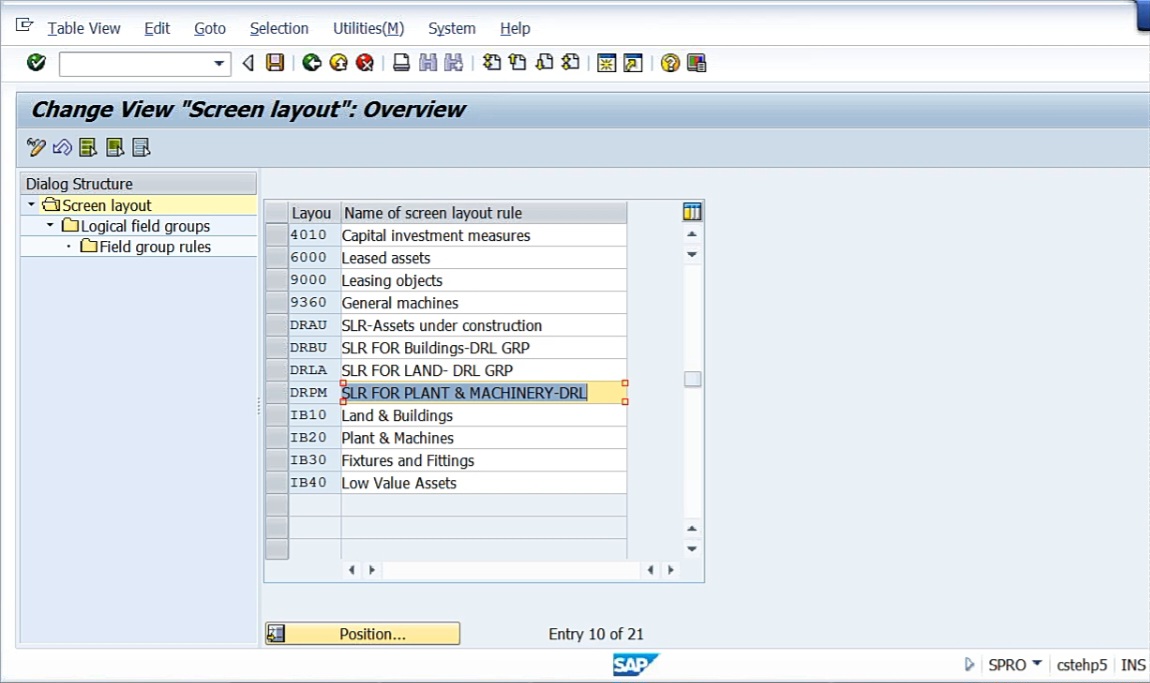

So here, Define Screen Layout For Asset Master Data. So this kind of screen layout we have seen at several places. OBC4 GL screen layout. Like that we have vendor screen layout and customer screen layout. While creating the groups, we have already created those groups. Even here in case of asset accounting, we will have some screens asset master records. Those screens will be controlled from here. Say for example, go to T-code AS02.

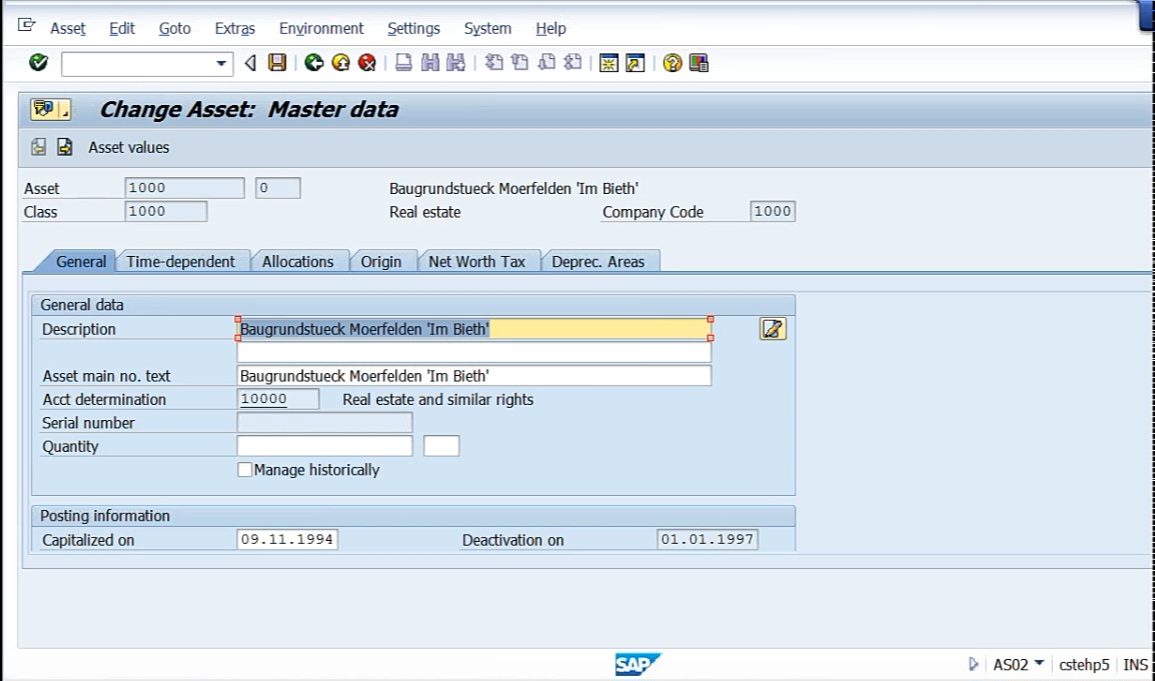

Here we do not have anything. Let me show you for 1000 company code, we have an asset.

So here, define screen layout for asset master data. The screen layout which we have created earlier, that is in the 6th and 7th step, the same thing is visible here. Screen layout rule for asset under construction.

Whatever the fields we have in the change asset: master data, all these fields are controlled from the change view “screen layout”: overview. How we control, I’ll show you. First one say for example Dr Reddy Labs, BU means building. Select building layout. Double click on logical field groups.

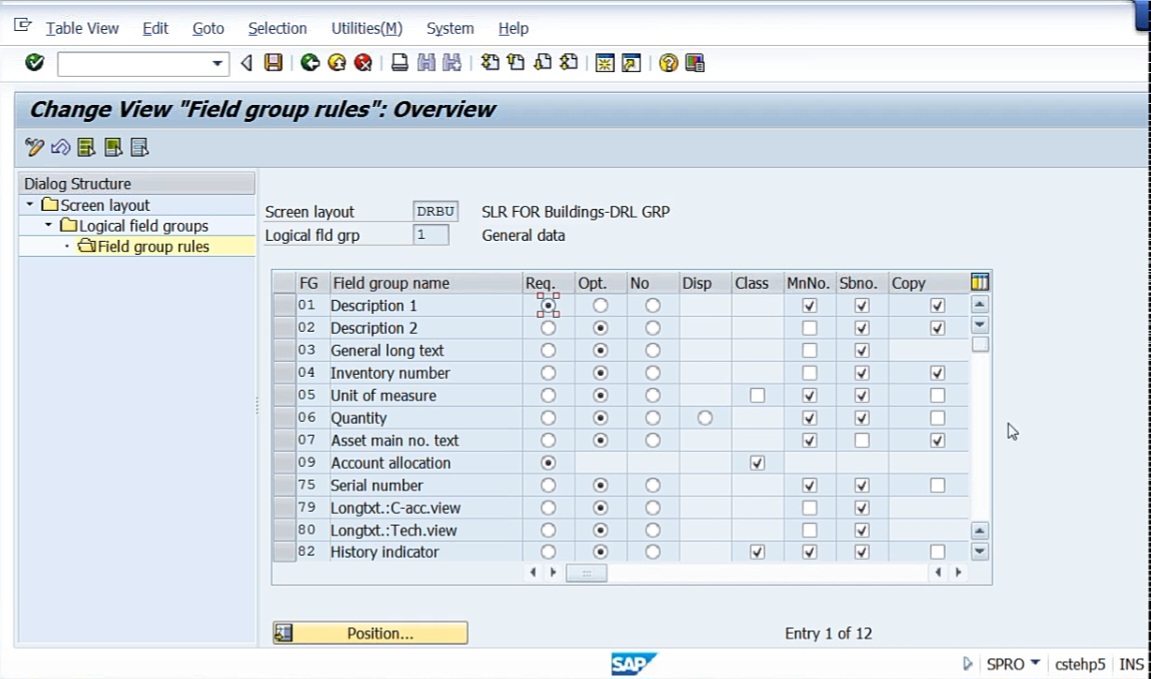

Here we have general data, posting information, time dependent data, allocations, like that. If you observe here, general data, posting information, time dependent, allocations, origin, all these fields are logical field groups. So these groups are these things. See general data, posting information, time dependent. Now again in general data, select general data, click on field group rules.

Here, so many things are there. Don’t disturb anything unless we know it. Description 1 required means here at the time of entry, the description should be system will ask compulsory, it will become mandatory field. When compared to posting information, time dependent data, this is important. In time dependent data, everything should be in optional mode, should not have cost center because we do not have any cost centers. Go back. Then select screen layout rule for Assets Under Construction, click logical field groups, general data we’ll take. Description 1 required entry. You have to check first time dependent data. If it is cost center required entry, make it optional entry. Because we cannot create cost center now because unless you create the controlling area etc, we cannot do that. But like this you have to see that in the time dependent data, nothing should be, that is cost center should not be mandatory, that is required entry. Come back. Then coming to land, logical field groups. Our concern is mainly time dependent data. Here, cost center should not be required entry, let us make it optional entry. For plant and machinery. Also select logical field groups. Here, under general data, description should be required entry whereas under time dependent, cost center should be changed from required entry to optional entry. Nowhere, don’t keep the cost center required entry because we cannot do that unless we create a controlling area. Save it.

So here, what are the screen layout rules that we have created? For each layout rule, we have adjusted that whether it is a required entry or optional entry, etc. You need not touch anything except because all the field status that’s the radio buttons etc, they’re arranged as per the requirement of the client, the standard requirement. But cost center, we have removed it, the reason being, we cannot create cost center unless we have a controlling area completely. So that’s why what I’ve done is, that I have not activated, that is required entry was made optional entry. So here with this we have completed the screen layout rules. Here, of course, we need not do anything. Define screen layout for asset depreciation areas.

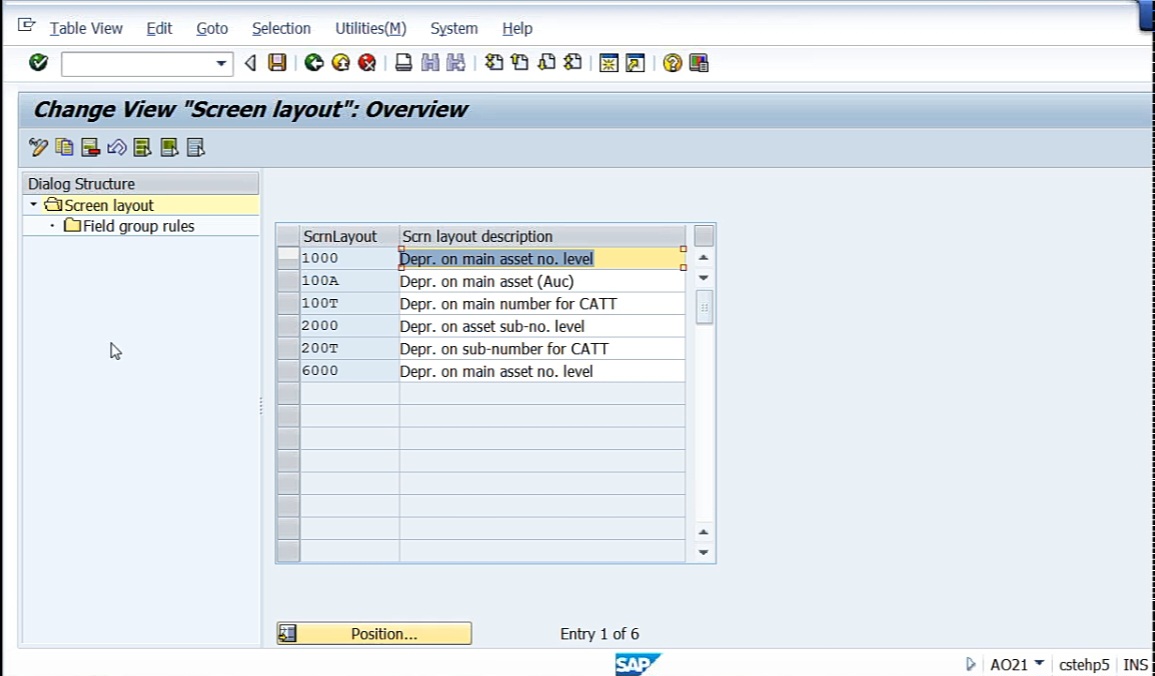

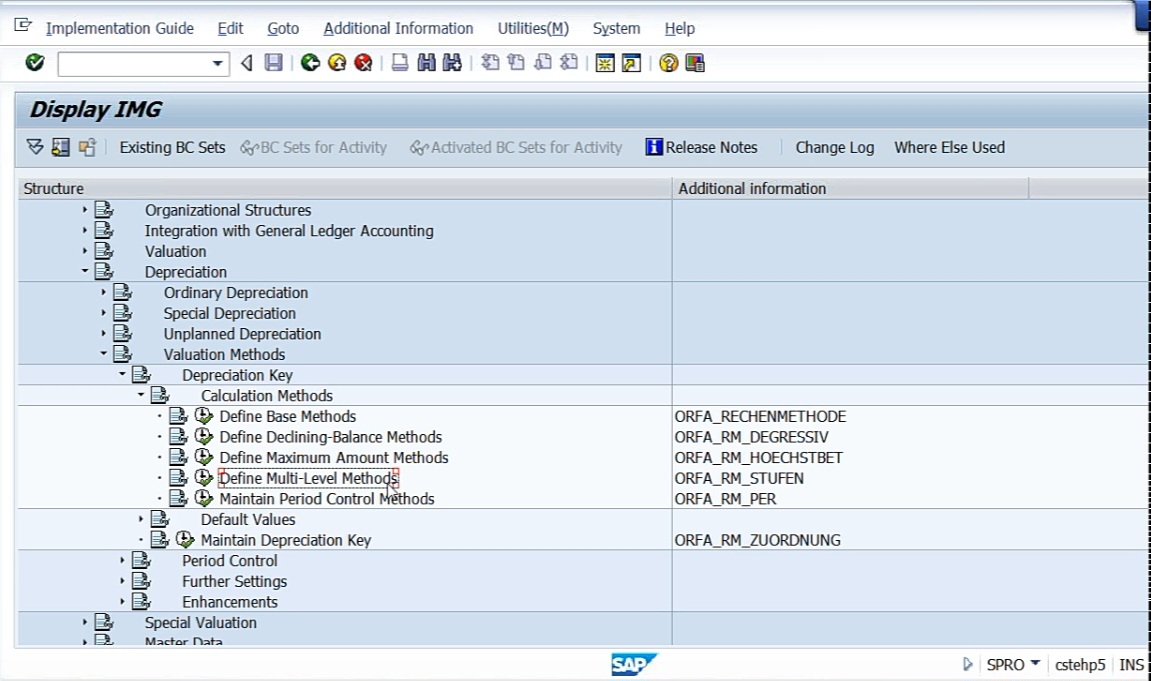

1,000 and 2,000. So these two, we are going to use depreciation on main asset number level, depreciation on sub asset number level. Anyhow, we’ll see that later. And here also we’ll have so many field status groups. Then coming to depreciation. We have ordinary depreciation, special depreciation, unplanned depreciation, valuation methods. Go to valuation methods, depreciation key, calculation methods. Here we have Define base methods, Define declining-balance methods, Define maximum amount methods, Define multilevel methods.

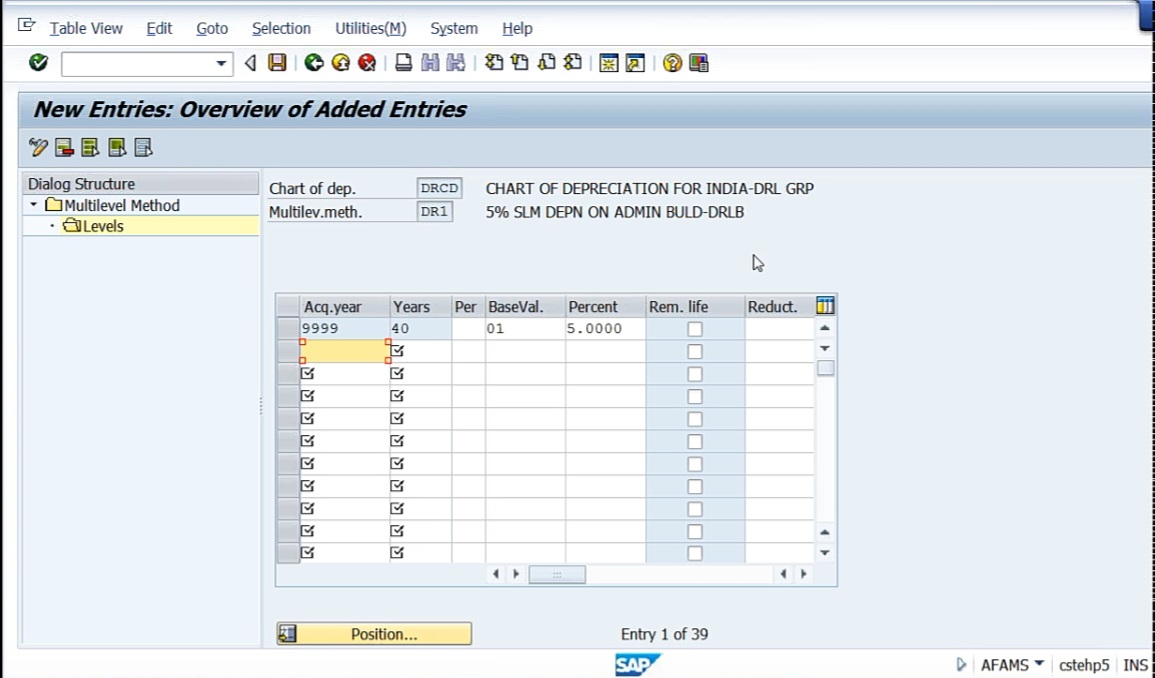

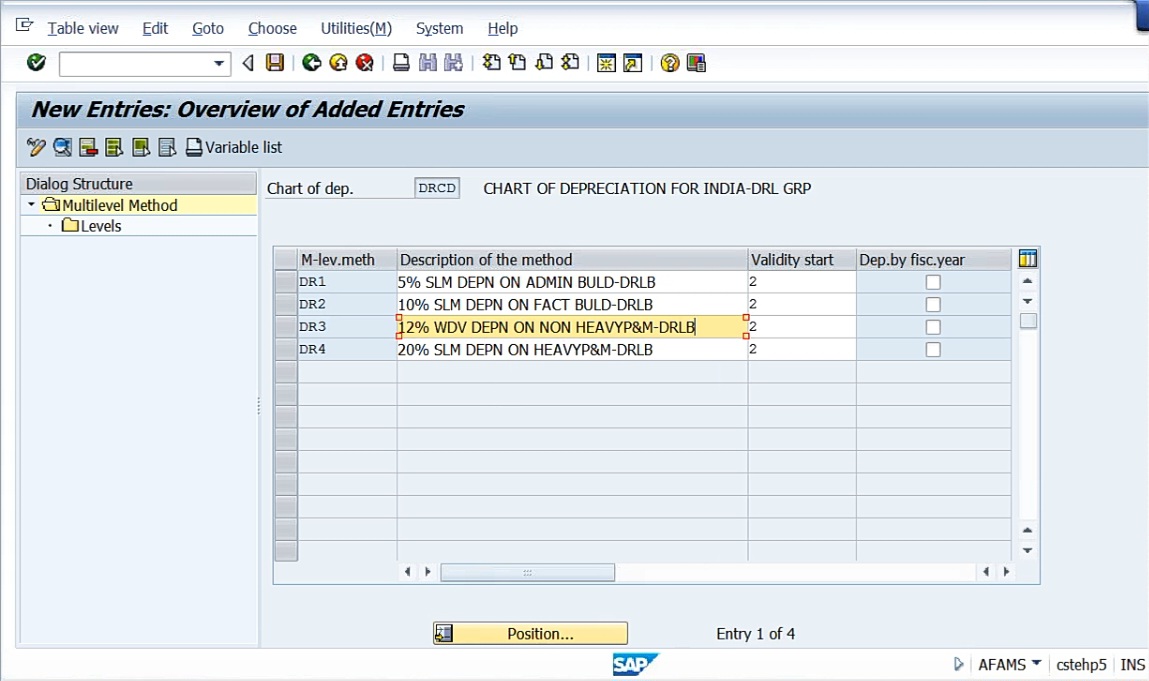

So here, define multilevel methods, this is important. We are going to create a multilevel method key. Click on this. So purpose everything I’ll tell you. First, go to new entries. And I need to define one key number. I’m taking this as DR1, that is Doctor Reddy Labs number 1 key. What is this? 5% straight line depreciation on admin buildings for Doctor Reddy Labs. This is the description part. I’m telling the system 5% depreciation on admin buildings. So this is the first key material method, Dr Reddy Labs.

Validity starts from ordinary depreciation start date means this rule of 5% depreciation should be applicable from the ordinary depreciation start date. Whenever the ordinary depreciation start date is there, from that date onward, that percentage is applicable. But when that date is applicable, nothing but the date of procurement or the date of put to use, whatever it may be, that’ll be the depreciation start date. Next go to Levels. Here we have multilevel method key. The name itself is multilevel method. Go to new entries. Here, acquisition year. Acquisition year means I don’t know when I’m going to acquire a particular asset. So that’s why what I’m doing here, acquisition year maybe any year up to 9999. So here, again, it’s asking for years. There’s acquisition year, there’s year. So this, straight line 5% straight line method depreciation on admin building. So for this, how many years? Okay. Let me take say 40 years. ‘Per’ means period. Here, base value, I should tell you. 01 acquisition value, percentage, 5%.

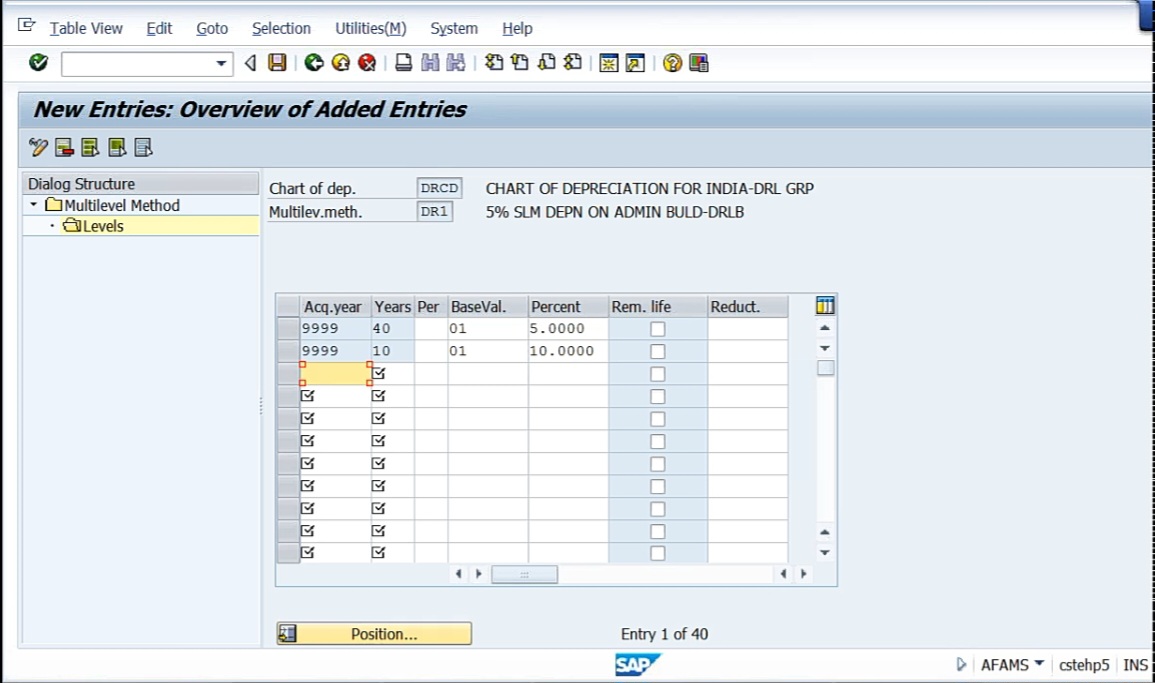

So what is this? So the meaning of this line is an asset see, 5% depreciation key I’m preparing. For this depreciation key 5%, technically system calculate 5% from here. And this is base value. What is meant by base value? 01 means acquisition value. So we are telling to the system, you calculate 5% on acquisition value. And for 40 years this depreciation key is going to be applicable. And 9999, so this rule will be applicable for up to 9999 years. That is the main meaning. And one more thing what we can do here actually, let me save here first. What I can do, multilevel method, the meaning of multilevel method is that acquisition year year, okay now up to 9999, I can take next acquisition year 9999. Then for years, I can say next 10 years. I can say 01 depreciation key, and I can say 10% depreciation.

So what we can do? After 40 years, next 10 years, I can say I can calculate depreciation at 10%. Because, after some time, asset will get depreciated at a faster rate. That’s what we can do. So that’s why multilevel method. But, of course in India, we don’t use this, but the system has given a provision. But I’m removing this second line, I’m not going to keep it. So this is nothing but the depreciation key. DR1 represents 5% depreciation on base value means acquisition value. System is going to calculate depreciation on the acquisition value. So we are asking the system to calculate 5% depreciation on acquisition value for 40 years. Asset may be procured in any year up to 9999 years. That is the meaning. Come back.

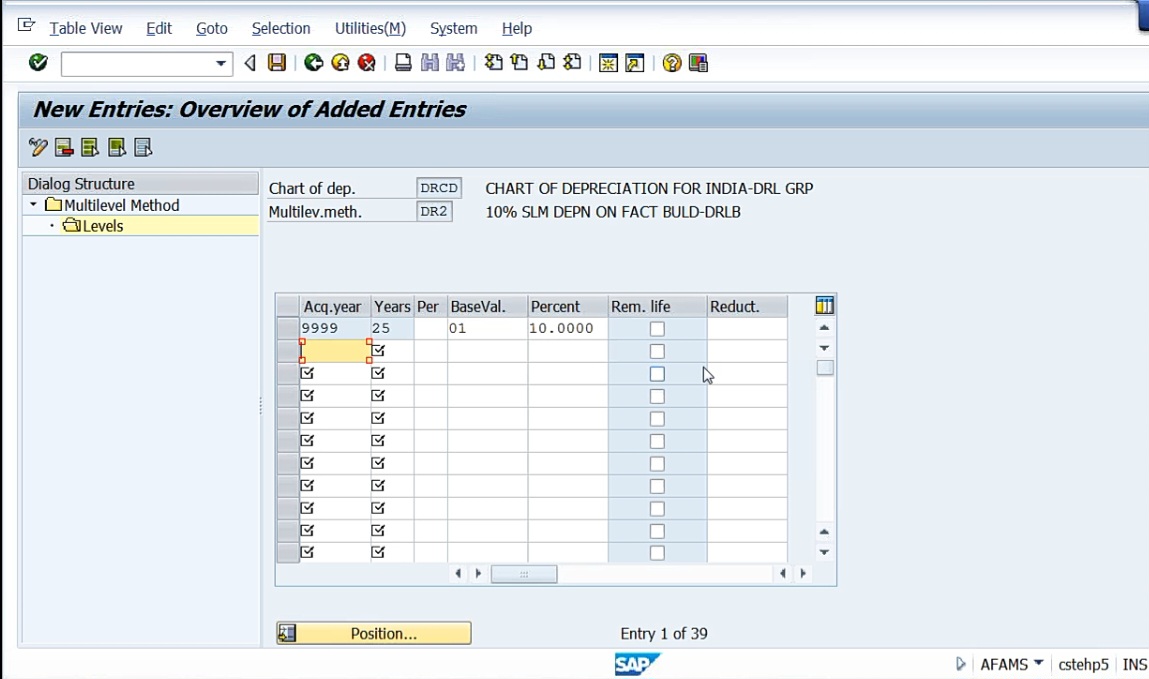

Next. I want to create one more key. DR2. 10% straight line depreciation on factory building. Because 5% straight line depreciation on admin building, on factory building generally the rate of depreciation will be high. Say DR2, 10% straight line method depreciation. Now what is meant by straight line method and what is the other method? Here straight line method means I think you might have studied this in bcom. Straight line method means every year, we provide same rate of depreciation. Here, that is straight line method. Here, I’ll tell you a little. Let me complete this and then I’ll tell you. Validity start date, same ordinary depreciation start date. Levels are going to be the same. Yet, say, for example, factory building this is. So factory building cannot stay, say more than 25 years, not possible. Say 25. Period means nothing but, say, 25 years, 6 months, I can use like that. Base value again, 01. Percentage, 10%. Save it.

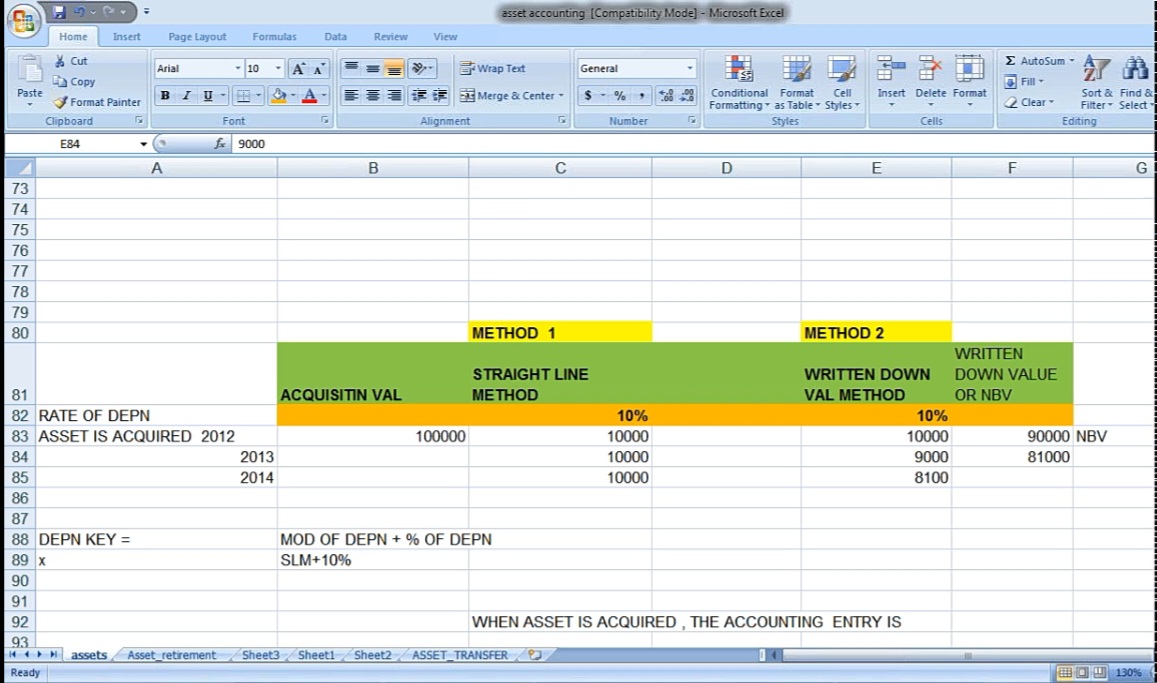

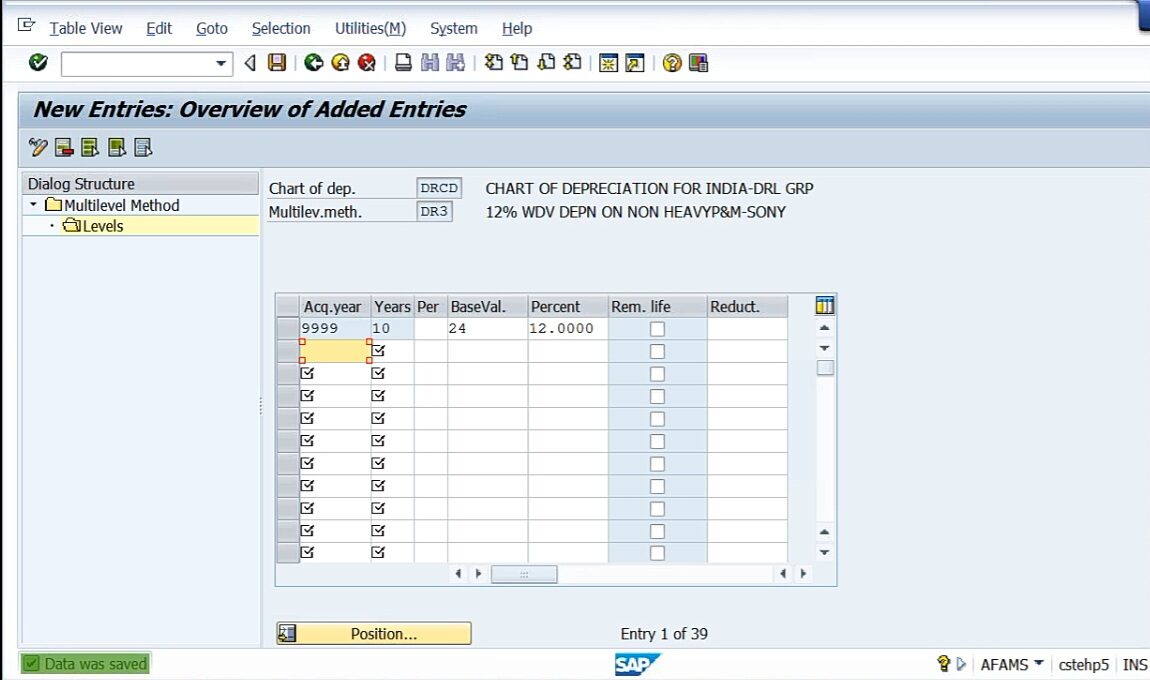

Come back. Next entry, 12% WDV depreciation. See here, I want to show you, straight line method, WDV, both. So here, 12% WDV. WDV means return down value method. SLM means straight line method. So straight line method is nothing but every year we provide depreciation on straight line basis. That is, say for example, 10%, every year 10%, it will calculate on original cost of the asset. But whereas in case of WDV method, system will calculate depreciation on the reduced value of depreciation. Remember that. See here.

Straight line method of depreciation and Return down value method of depreciation. In straight line method, we calculate depreciation on the original acquisition value. But whereas in case of return down value method, depreciation is calculated on the return down value. Say for example, rate of depreciation 10%. Now asset acquired, say for example in 2012. First year depreciation is how much? 10% on original acquisition value. In 2013, same, that is 10% on 1 lakh. So in 2014, same 10,000. But whereas in case of return down value method, first year 10000, 10% and, net book value. Net book value means asset value minus depreciation is nothing but net book value, NBV. So NBV will be 90,000. Asset original cost 1 lakh minus 10,000 is 90,000. Now on 90,000, next year depreciation, now the net book value. So we have to calculate 10% on net book value, that is 9,000. Say second line, 9,000. So like this, every year when you calculate depreciation, depreciation is going to be calculated on the net book value here. But whereas in the straight line method, on the original value we calculate depreciation. That’s why every year 10,000. But whereas here in WDV, 1 lakh minus 10,000, 90,000. And on 90,000 minus 9,000, 81,000. 81,000 minus 8,100 there is a depreciation. So like this, every year depreciation will get reduced. This is called WDV method.

So like this, we are creating the deprecation key. And the next is DR3. 12% WDV depreciation on non heavy plant and machinery. I want to show you how depreciation is going to be calculated on WDV method also. Go to Levels, select new entries here. Say for example, non heavy plant and machinery. Say for example, 10 years. Percentage is 12%, and base value is nothing but net book value, that is 24 is net book value.

That means what? System is going to calculate 12% on netbook value. What is netbook value? Here 90,000 is the netbook value. Right. I’m asking the system to calculate the depreciation on the net book value not on original cost. But in SLM on the original cost always, 01 acquisition cost. But here net book value. So 24 is net book value. So we are telling to the system, you calculate 12% depreciation on net book value. So there is the meaning.

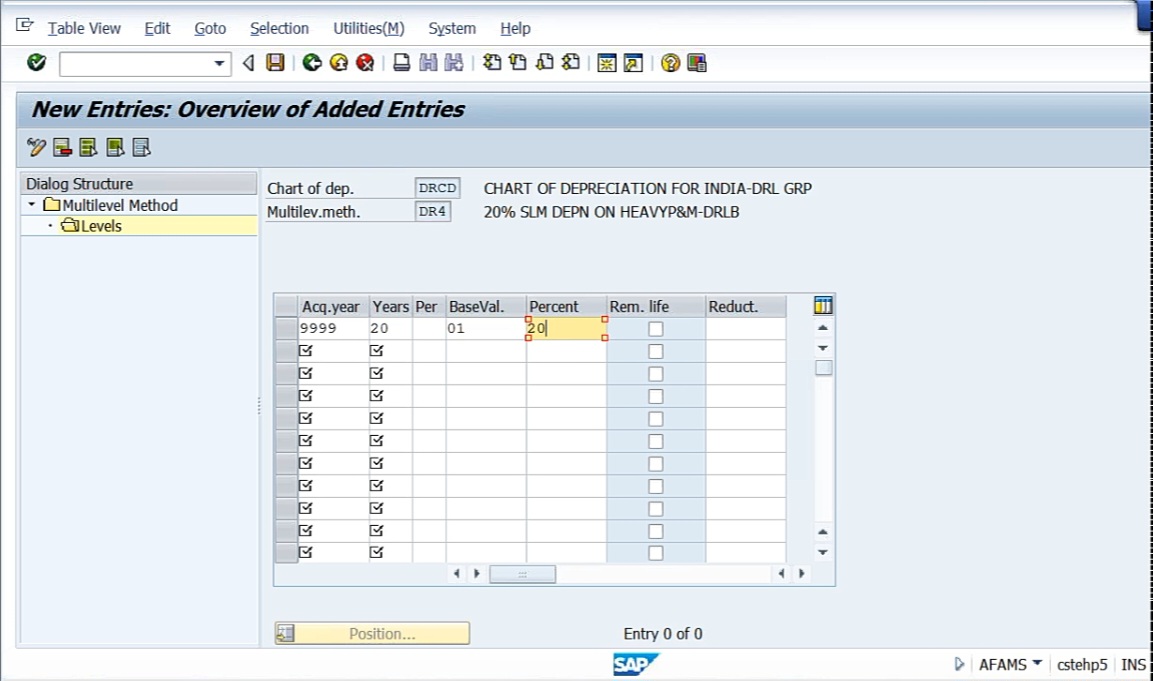

Next, DR4. That is nothing but 20% straight line method depreciation on heavy plant and machinery. Go to Levels, then New entries. So heavy plant and machinery say 20 years I’ll take. Base value, so WDE method or straight line method. Here let’s say acquisition value, means original cost of the asset. So we are asking the system to calculate depreciation on original cost of the asset. Original cost means original acquisition rate. Here I’m taking 20%.

So we have created 4 depreciation keys. DR1, 2, 3, 4. 5%, 10%, 12%, 20%.

So these are the 4 depreciation keys we have created. Let us stop here today.